If you took advantage of forbearance due to hardship, there are several options moving forward.

With the unemployment rate above 13% since COVID-19 shutdowns began in mid-March, many Americans have turned to mortgage payment relief programs to help manage their short-term cash flow problems.

In fact, the total number of home loans now in forbearance increased to 8.36% according a recent report from the Mortgage Bankers Association. But a Fannie Mae survey revealed that only half of mortgage holders understand what forbearance actually is.

In short, forbearance is when your mortgage lender allows you to pause your payments for a limited period of time. Forbearance does not erase what you owe, but rather delays those payments to provide borrowers time to recover from financial hardship.

Lenders most commonly make forbearance options available to borrowers following events like natural disasters – in this case, the global pandemic triggered a national need for assistance.

Through the Coronavirus Aid, Relief, and Economic Security (CARES) Act, which went into effect in late March, the federal government provided forbearance options for borrowers with federally-backed mortgages. If a homeowner's mortgage is backed by Fannie Mae, Freddie Mac or another government entity, they can pause their mortgage payments for up to 180 days and request an additional 180 days if needed.

In addition to providing assistance for loans we service for Fannie Mae and Freddie Mac per the CARES Act, we are also offering forbearance options through TD Cares for residential mortgage and home equity loans and lines that we own and service, in increments of 90 days up to one year.

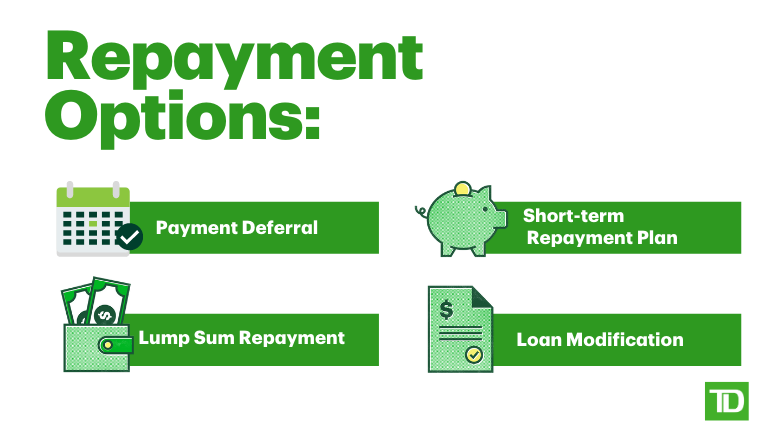

Repayment Options

Many lenders, including TD, are offering repayment options consistent with the general guidelines established by Fannie Mae and Freddie Mac. But determining which option is best for a particular borrower requires assessing their individual situation once their financial hardship is resolved.

TD is contacting all borrowers in forbearance after the first 60 days to determine if they're still impacted and what their intentions are for repayment, which could include but is not limited to extending their forbearance period or beginning discussions about repayment. As the first wave of borrowers seeking payment relief began their forbearance period in April, many are in the process of determining their next steps.

- Payment deferral: The borrower can move the missed payments to the end of the loan term. Those payments would still accrue interest and when the loan reaches maturity, the borrower would make a balloon payment (a single lump sum payment).

- Lump Sum Repayment: The borrower can pay the total amount of the missed payments in a lump sum at the end of the forbearance period.

- A short-term repayment plan: The borrower can repay in smaller, more manageable payments over the course of six months.

- Loan modification: The terms of the loan can be modified based on needs and eligibility, and may include adjustments to the term of the loan, interest rate and loan type.

"Over the past several weeks, we have had all hands-on deck to handle the influx of calls from customers who are understandably concerned and turning to TD for help," said Steve Kaminski, Head of U.S. Residential Lending at TD Bank. "We have re-allocated resources to our response teams and appreciate all of our Colleagues' efforts in delivering clarity and assistance to our borrowers in the midst of these challenging times. We believe it's critically important for our Customers to understand their options."